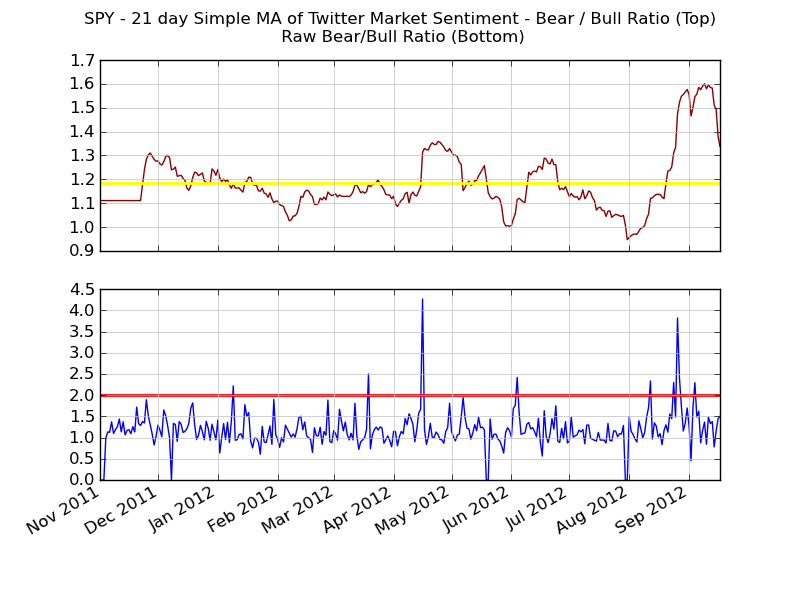

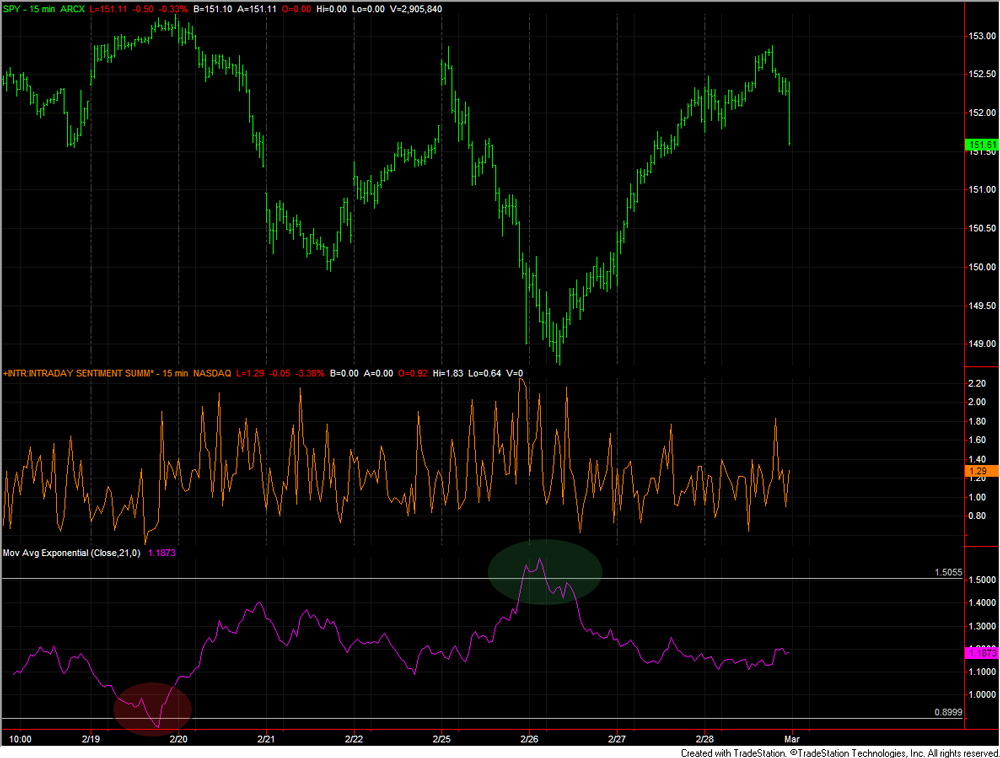

Using Twitter Sentiment for Intraday Signals

This is a cross-post from Trade The Sentiment. Originally published as Using Twitter Sentiment for Intraday Signals.

While most of my research on Twitter Sentiment has been for use on larger time-frames (Daily, Weekly, etc), I’ve been very curious about using sentiment for intraday signals.

I finally found some